Money looks simple—a rupee note, a bank balance, a UPI tap. In reality, India’s financial life runs on a currency operating system: RBI policy, bank credit creation, domestic payment rails, global USD flows, and a tokenized future via e₹.

Table of Contents

- The Money Stack

- From Gold to Fiat to Floating Rates

- Why the USD Still Moves the INR

- INR’s Exchange-Rate Regime: Managed Float

- e₹ vs Digital Currencies

- How Tokenization Reduces Fraud

- FAQs

- Sources (Verified & Authoritative)

- Disclaimer

1) The Money Stack

Layer 1 — Legal Tender (₹): The RBI Act, 1934 empowers the Reserve Bank of India to issue banknotes and manage the monetary system.

Layer 2 — RBI: Sets the policy rate, manages liquidity via OMO/QE/QT when needed, supervises banks, and maintains orderly markets under a managed float for INR.

Layer 3 — Commercial Banks: Most money is created when banks extend credit, simultaneously creating matching deposits; money is destroyed as loans are repaid.

Layer 4 — Payments Layer: UPI/IMPS/cards are the consumer interface that moves claims on bank deposits quickly and at low cost.

Layer 5 — Tokenized Layer (Future): BIS proposes a tokenized unified ledger integrating central bank reserves, commercial bank money, and government bonds for atomic, programmable settlement; RBI pilots e₹.

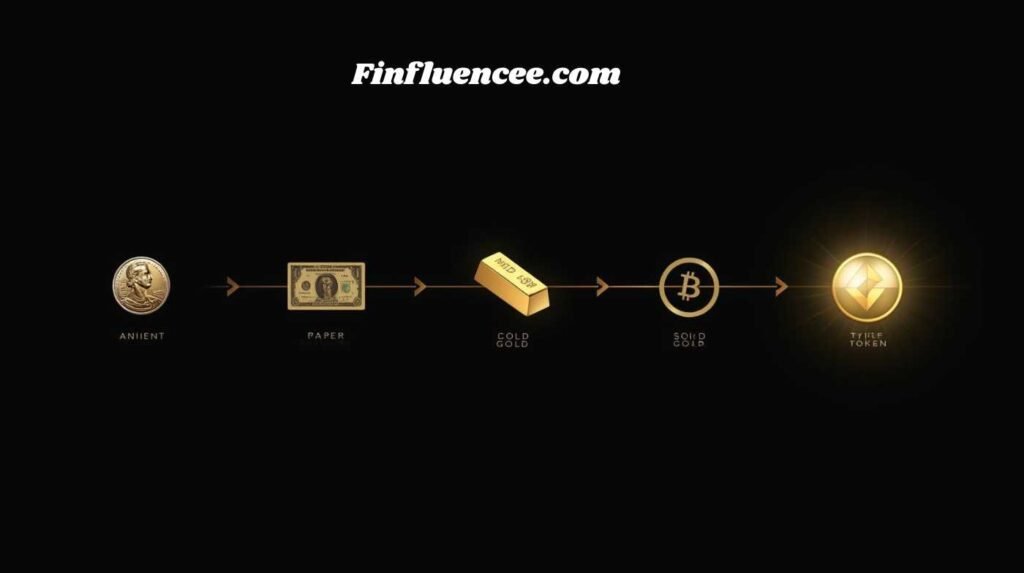

2) From Gold to Fiat to Floating Rates (Evolution of Money: A Brief Timeline)

• Coins standardize value (Lydia, ~7th c. BCE).

• China’s Song dynasty issues paper notes (11th c.).

• Bretton Woods (1944) fixes USD to gold at $35/oz and pegs other currencies to USD.

• The 1971 Nixon Shock ends convertibility; by 1973 major currencies float. Policy flexibility replaces metal backing.

3) Why the USD Still Moves the INR

The USD dominates FX turnover, official reserves, international debt markets, and payments far in excess of the US share of global GDP/trade. Dollar cycles transmit through funding conditions and risk appetite, affecting INR.

Action (for Indians with USD outflows): ladder conversions over 3–6 months rather than one-shot buys; align with known payment dates. (Educational only.)

4) INR’s Exchange-Rate Regime: Managed Float

India is not a hard peg. The rupee is largely market-determined; the RBI intervenes mainly to reduce excess volatility and maintain orderly conditions, not to defend a fixed level.

5) e₹ vs Digital Currencies

What e₹ is: A Central Bank Digital Currency legal tender in digital form, issued by RBI, equal in value to cash, with pilots for retail/wholesale, offline mode, and programmability.

What e₹ is not: Not a cryptocurrency, not a private stablecoin, not a replacement for bank deposits or UPI. It complements existing rails and banking.

Cryptocurrencies: Private, volatile, not legal tender, not backed by a central bank. Stablecoins: Private claims pegged to fiat; BIS finds they fail tests of singleness, elasticity, and integrity for core money.

6) How Tokenization Reduces Fraud

• Atomic settlement: Combines messaging, reconciliation, and settlement into one programmable step, leaving no timing gap for instruction tampering.

• Immutable audit trails: On-ledger records are tamper-evident, improving forensic visibility and reducing back-dating or unauthorized edits.

• Double-spend prevention: Token uniqueness plus cryptographic signing prevents duplication of value.

• Permissioned access & identity: CBDC/tokenized platforms assign verified participants and role-based permissions, reducing account takeovers and insider fraud.

• Programmability: Purpose-bound transfers (e.g., subsidies) can enforce usage constraints or expiry cutting leakage.

FAQs

Q: Is fiat real without gold?

Yes—modern currency’s value is anchored by law, taxation, institutional credibility, and policy. Gold convertibility ended globally in 1971.

Q: Who creates most money?

Commercial banks via lending; policy/regulation constrain this engine.

Q: Will e₹ replace UPI?

No. e₹ complements bank money and UPI rails.

Sources (Verified & Authoritative)

• Reserve Bank of India – Brief History

• RBI Act, 1934 (Official India Code PDF)

• RBI – Digital Rupee (e₹) FAQs (Updated Feb 4, 2026)

• Bank of England – Money Creation in the Modern Economy (2014 Q1)

• Federal Reserve – International Role of the U.S. Dollar (2025 Edition)

• Federal Reserve History – Creation of the Bretton Woods System

• Federal Reserve History – Nixon Ends Convertibility to Gold (1971)

• IOSCO – Tokenization of Financial Assets (Final Report, Nov 2025)

Disclaimer:

The content is for education and general information only. It is not financial, investment, tax, or legal advice. Always verify key information with official sources and consult a qualified professional before making financial decisions.

Puspanjali

March 16, 2026Nice explanation on currency will give better understanding

Lalatendu R Patra

March 16, 2026Thank you! Glad you found it helpful!!

Understanding how currency evolves—from gold to digital forms like the e₹—really changes the way we look at money in daily life. More such simple breakdowns coming soon!